The ongoing Iran conflict in 2026 is not just a geopolitical crisis or an energy shock. It may mark a turning point in the global financial system itself. At the heart of this shift lies the petrodollar system—a decades-old arrangement that has sustained the dominance of the US dollar in global trade. Today, with Iran leveraging oil flows through the Strait of Hormuz and experimenting with non-dollar settlements, the very foundations of that system are being tested.

To understand the stakes, one must go back to the mid-20th century. After World War II, the global monetary order was established under the Bretton Woods system, where currencies were pegged to the US dollar, and the dollar itself was convertible to gold at $35 per ounce. This gave the dollar unparalleled credibility and made it the backbone of global trade.

However, in 1971, President Richard Nixon ended the dollar’s convertibility into gold, effectively dismantling Bretton Woods. The dollar became a fiat currency, backed not by gold but by trust in the US economy and its institutions.

At that moment, the dollar needed a new anchor. That anchor became oil. In 1974, the United States struck a historic deal with Saudi Arabia. Under this arrangement, Saudi Arabia agreed to price its oil exclusively in US dollars and invest surplus revenues into US financial assets, particularly Treasury bonds. In return, the US provided military protection and security guarantees.

This agreement was later adopted across much of OPEC, creating what we now call the petrodollar system.

The implications were profound:

- Countries worldwide needed dollars to buy oil

- Global trade began to be invoiced in dollars

- Central banks accumulated dollar reserves

- Oil exporters recycled their earnings into US assets

The concept of “the world saves in dollars because it pays in dollars” came into picture with oil being the central link in that chain. This system entrenched the dollar as the world’s reserve currency, allowing the US to run persistent trade deficits while maintaining global demand for its currency.Oil’s central role made this system particularly resilient. It is embedded in nearly every aspect of modern life, from transportation to manufacturing to agriculture. Because oil is priced in dollars, companies across supply chains prefer to price their goods in dollars as well, creating a self-reinforcing loop. The more the world trades in dollars, the more it saves in dollars, and the stronger the system becomes.

Oil’s central role made this system particularly resilient. It is embedded in nearly every aspect of modern life, from transportation to manufacturing to agriculture. Because oil is priced in dollars, companies across supply chains prefer to price their goods in dollars as well, creating a self-reinforcing loop. The more the world trades in dollars, the more it saves in dollars, and the stronger the system becomes.

But this system was already weakening long before the Iran conflict brought those cracks into the spotlight. The global energy landscape has shifted significantly over the past two decades. The United States is no longer the primary buyer of Middle Eastern oil, with Asia now accounting for the majority of demand. Countries like China have been exploring alternatives to dollar-based trade, while sanctioned nations such as Iran and Russia have already been conducting oil transactions outside the dollar system. New financial infrastructure, including digital currency platforms and bilateral trade agreements, has been slowly reducing reliance on traditional dollar channels.

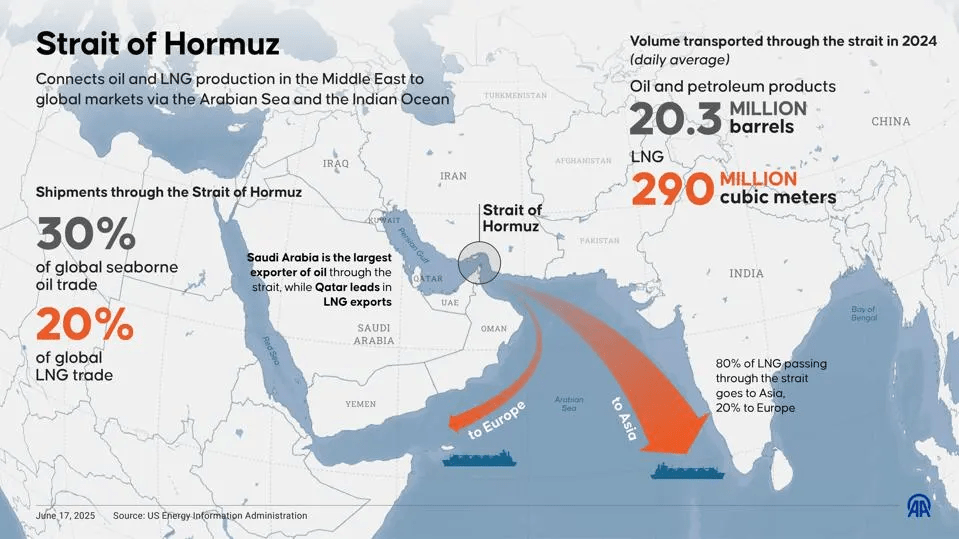

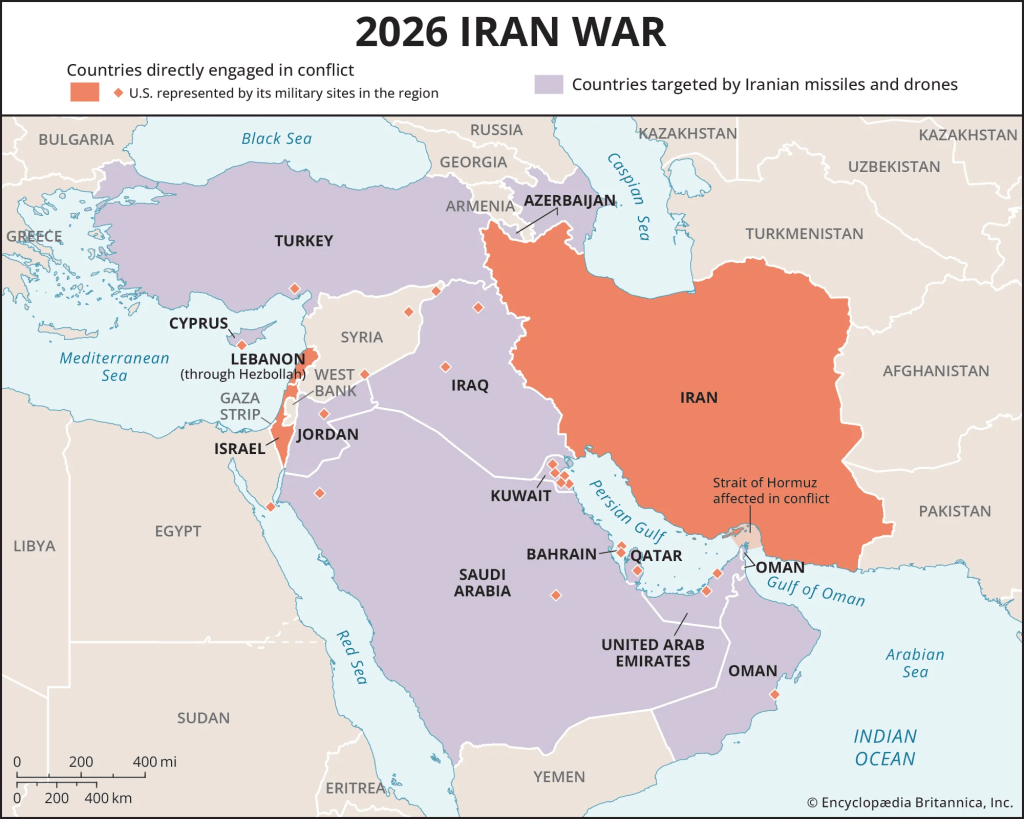

The 2026 Iran conflict has disrupted global energy flows at a scale comparable to the 1970s oil crises. The closure or restriction of the Strait of Hormuz, through which roughly 20% of global oil passes, has triggered supply shocks, price spikes, and economic instability. More importantly, Iran has introduced a new strategic weapon: currency.

Reports suggest that Iran has considered allowing oil shipments through Hormuz only if transactions are settled in Chinese yuan instead of US dollars. This is not just a challenge to the petrodollar system, it is the first credible attempt in decades to bypass it at scale. Such moves could “accelerate de-dollarisation” and reshape global finance. Currencies don’t dominate by accident, they dominate by necessity.

If oil begins to be priced in currencies like the Chinese yuan, the consequences could be transformative.

China has already been working toward this goal:

- It is the largest importer of oil

- It has established yuan-based oil contracts

- It has built alternative payment systems to bypass the dollar

This emerging system is often referred to as the petroyuan.

The Iran war provides the perfect opportunity for its expansion:

- Countries dependent on Middle Eastern oil may be forced to adopt yuan payments

- Sanctioned states gain a way to bypass US financial systems

- Energy trade begins fragmenting into multiple currency blocs

At the same time, the conflict has exposed vulnerabilities in the longstanding relationship between oil producers and US security guarantees. The stability of the petrodollar system has always depended on a broader geopolitical framework, where the United States ensured the security of key energy routes and infrastructure. Recent events have raised questions about how reliable that framework remains. Attacks on infrastructure, disruptions to shipping lanes, and the increasing complexity of regional alliances suggest that the old model may no longer be as secure as it once was.

If oil-producing nations begin to reassess their strategic alignments, they may also reconsider the currencies in which they conduct trade. Even a partial shift away from the dollar could have significant consequences. Global demand for dollars is not just about confidence, but about necessity. If fewer transactions require dollars, fewer reserves need to be held in dollars.

The implications extend beyond currency markets. For decades, the recycling of oil revenues into US financial assets has played a crucial role in financing American deficits. If that cycle weakens, it could lead to higher borrowing costs and increased financial volatility. The dollar is unlikely to lose its status overnight, but its dominance could gradually erode.

There is also a deeper, structural force at play that could prove even more transformative: the global transition in energy itself. The current crisis may accelerate efforts to reduce dependence on imported fossil fuels. Countries that are heavily reliant on external energy sources are already exploring alternatives, including renewables, nuclear power, and domestic production. These shifts are driven not just by environmental concerns, but by the desire for energy security.

If the world begins to rely less on globally traded oil, the foundation of the petrodollar system weakens from another direction. The system depends not only on the currency in which oil is priced, but on the scale of oil trade itself. A reduction in global oil trade would naturally reduce the role of the dollar in international transactions.

This creates a scenario where both pillars of the system are under pressure. On one side, there is the possibility of oil being priced in alternative currencies. On the other, there is the possibility of reduced reliance on oil altogether. Together, these forces represent a significant challenge to a system that has remained largely intact for over half a century.

None of this suggests an immediate collapse of the dollar’s role. The dollar remains deeply embedded in global finance, supported by strong institutions, deep capital markets, and widespread trust. But the current moment feels different. For the first time in decades, the mechanisms that sustain dollar dominance are being questioned simultaneously from multiple directions.

The Iran conflict may ultimately be remembered not just as a regional war, but as a catalyst for a broader transformation. It has highlighted how closely intertwined geopolitics, energy, and finance have become. It has also shown that control over physical resources can translate into influence over financial systems.

What emerges from this period may not be a single replacement for the dollar, but a more fragmented global system, where multiple currencies coexist and compete. Trade may become more regional, alliances more fluid, and financial flows more complex. In such a world, the dominance of any single currency becomes harder to sustain.

For decades, the petrodollar system has quietly underpinned global economic stability. Today, it stands at a crossroads. The outcome will depend not just on the resolution of the Iran conflict, but on how nations respond to the deeper questions it has raised about energy, security, and the future of money. The dollar’s power was never just economic, it was engineered.